If you’re considering a new deck or a roof replacement, you might think twice before you cut once.

It turns out that the cost of a roof is, well, through the roof.

Douglas fir prices have doubled.

Some plywood prices have nearly quadrupled.

Lumber prices are up over 200%

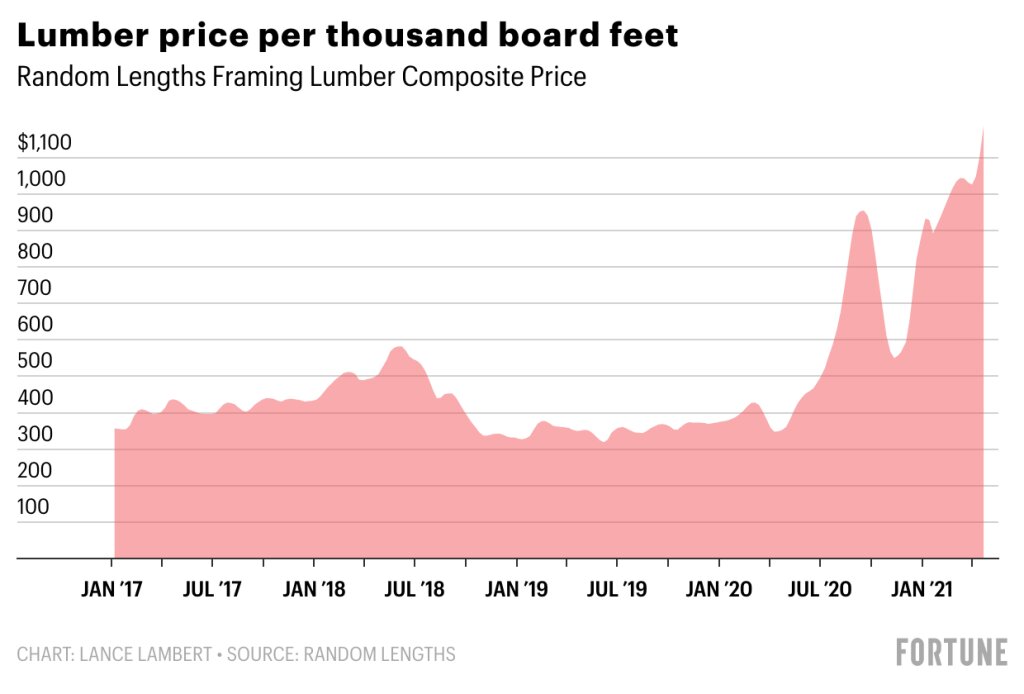

Last week the price per thousand board feet of lumber soared to an all-time high of $1,188, according to Random Lengths. Since the onset of the pandemic, lumber has shot up a whopping 232%.

Home builders and DIYers don’t want to hear this, but the ceiling could be higher—maybe even a lot higher. Last Monday, the May futures contract price per thousand board feet of two-by-fours jumped from $48 to $1,420. That squeeze once again triggered the circuit breakers and caused lumber trading to halt for the day. Why would lumber yards and builders pay above market rates? Severe lumber scarcity has buyers on edge. They’re buying the sky-high contracts in order to ensure they’ll actually get the lumber they need for projects already under contract.

“The market is in trouble. It could spiral out of control in the next few months,” Dustin Jalbert, senior economist at Fastmarkets RISI, said. The issue? Supply, which is already backlogged, simply can’t catch up as demand continues to grow with the start of the home building and home renovation seasons.

This supply and demand mismatch is largely a result of the pandemic. At the same time that state-mandated lock downs caused mills to halt production, bored quarantining Americans were rushing to Home Depot and Lowe’s to buy up materials for do-it-yourself projects. That caused lumber inventory to plummet. It only got worse from there: Recession-induced record-low interest rates caused a housing boom. In March, new housing starts hit their highest levels since 2006. Of course, new homes require a lot of lumber, thus exacerbating the shortage.

This supply and demand mismatch is largely a result of the pandemic. At the same time that state-mandated lock downs caused mills to halt production, bored quarantining Americans were rushing to Home Depot and Lowe’s to buy up materials for do-it-yourself projects. That caused lumber inventory to plummet. It only got worse from there: Recession-induced record-low interest rates caused a housing boom. In March, new housing starts hit their highest levels since 2006. Of course, new homes require a lot of lumber, thus exacerbating the shortage.

On the supply side, lumber production is finally rebounding: Wood production hit a 13-year high. But that can only do so much. Limited mill capacity combined with labor shortages, mean supply can’t catch up to robust demand.

Stinson Dean, CEO of Deacon Lumber, said on Monday that soaring lumber futures contracts, including for months as far away as November, signal that lumber prices will be elevated for quite some time.

For prices to correct, Jalbert says, demand will need to cool down—something that is unlikely to occur until the home building and renovation seasons are over. Simply put, exuberant lumber prices aren’t going anywhere in the next few months.

With interest rates as low as they are, it could be fairly tempting for a potential new home owner to jump in on the readily available financing for that new home construction loan only to be disappointed to see that the costs associated with most building materials have quite literally gone through the roof. Smaller home builders/contractors can put the bid in at the current price for materials and end up being turned down by the client once they experience the sticker shock related costs.

Larger builders/contractors might be willing to see their margins evaporate in the short term just to stay in the game. Knowing that these prices are totally unsustainable in the long term, they may be willing to risk the loss if it means better days being just around the corner will justify their short term red ink on the ledger books.

On yet another front, I can see the eventual potential loss of jobs in the industry as smaller builders/contractors struggle to close the gap between materials cost and profit. It seems as well that nobody seems to remember 2008-2009 when the housing market tanked. As with any bubble, it’s all going to come to a head eventually, and once again, regardless of the current low rates, home owners will once again be left holding the bag.

I see that the Fed has painted itself into another corner. Keeping interest rates insanely low does nothing for the economy, as the Fed will eventually have to raise rates thus creating another perfect storm of foreclosures as home owners suddenly realize that they are now upside down not only on their loans, but also on their hyper inflated property taxes related to those loans. They’ll be stuck having to pay huge money for a property/home that wasn’t really worth huge money to begin with.

As for me? As tempting as it might sound to run all off to the bank with my arm out and my leg up to get that “cheap” loan, I’ve opted to wait it out.

{kind=link}